[I]n this world nothing can be said to be certain, except death and taxes.

Benjamin Franklin Letter to Jean-Baptiste Leroy (13 November 1789); reported in Bartlett’s Familiar Quotations, 10th ed. (1919)

Yesterday when I wrote about income inequality it may have seemed like I implied the solution to the problem would only come when people in our society changed to be less greedy. That is not what I meant. There are actual concrete policy steps we can take now to help fix the symptom (income inequality) and the disease (unsatisfiable hunger). Tax reform is the first and most important step.

Taxes currently favor the rich, both in the manner of how income is determined, and then how income is taxed. Let’s tackle income first. When I was a lawyer I had a law office which I formed into a PC (professional Corporation). This meant that all the income I earned from the business was “passed through” to my personal income taxes (it was not subject to corporate tax and then personal tax). These are a lot like wages, except that as a business owner I get tax subsides for some of the things that a wage earner doesn’t get. An example is a car.

Most people on the west coast and many on the east coast have cars. Both wage earners and business owners would have these cars regardless of how the tax law treats them. But as a business owner I received some benefits that I didn’t receive when I was just a wage earner.

I would drive to see clients and I was able to deduct that percent of my car expenses. If 10% of my car’s usage was driving to clients I would be able to deduct 10% of my registration fees, insurance, repairs, tires, etc. One could argue that it’s fair to deduct repairs and tires because those could have been less if not for the work related driving. But registration and insurance would be the same. So if you use your car directly for work, like almost all business owners are able to claim to some degree, you receive a public tax subsidy. This deduction is a business expense, which as the IRS defines it is, “the cost of carrying on a trade or business.”

However, neither the business owner nor the wage earner is allowed to deduct the cost of commuting to work. This is a non-deductable expense. Yet no business would be able to carry on a business if it’s employees would not come to work. Thus we see one example of a tax benefit that primarily accrues to owners (typically the wealthy class) rather than workers.

Another example of a tax deduction that favors the well off rather than the average employee, is travel expenses related to training or education. One can attend a conference in Hawaii and deduct the airfare to and from, as well as the conference fees and food during the conference. Of course the costs you incur in the two weeks following aren’t a tax deduction, but who cares you got to Hawaii for “free” (your airfare was subsidized by tax breaks). This is a benefit that helps professionals and business owners rather than blue collar and minimum wage workers.

These examples are chump change compared to the more egregious discrepancy in what income is taxed, i.e. capital gains tax. For the most part capital gains (or losses) are the gains you make from selling stocks, businesses, and your home (although you can’t claim a loss on your personal home sale). In the past this income was taxed at 15%. Now there is a 20% rate on this income if the individual (married filing jointly) is in the 39.6% tax bracket.

The implications are huge. If you earn $1 million in taxable wage income you pay, $342,752.90 in taxes. But if you did not work and sold some stock for $1 million profit (profit=sale price – buy price) you would pay $150,000 in taxes. Of course if you have millions in investments you don’t need to sell them to get money, you borrow.

This is where the biggest discrepancy between the rich and the wage earners arise. They get to borrow money basically tax free while we are paying taxes on the money we earn to pay for the money we borrowed. The rich service their loans buy selling their investments which are offset by losses and have a tax rate of either 15 or 20%. Whereas the average middle class person pays their loans with their wages which are taxed 25 to 28%. Middle class in big cities might even pay 33% of their taxes, because the income needed to be middle class in cities is higher than other places

If you’re rich and you want $1 million in cash now you borrow it. I’m estimating Richie Rich can get a loan at 5%, which I bet is much higher than the super rich really have to pay to borrow (considering I can get $100k at 7% secured). That 5% works out to $10,600 per month about $127k per year. So Richie Rich sells stock for $150K profit at 15% capital gains tax and nets out that $127k needed to service the 1st year of that million dollar loan. Not to mention Richie probably has some stock losses that can be sold to offset the gains from other stocks, thus in effect getting the gains tax free.

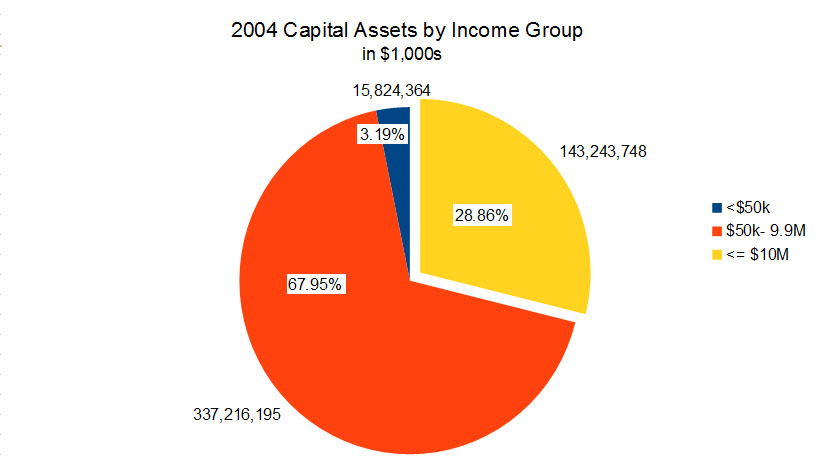

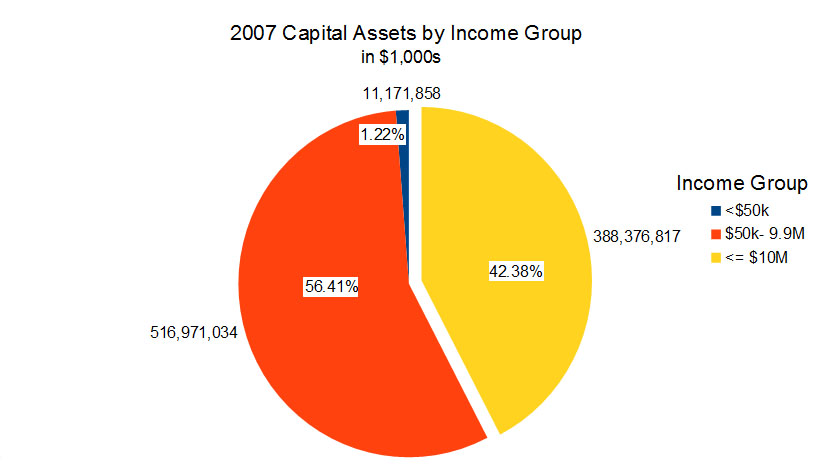

One more little bit on the number involved then we can move on to solutions. The IRS did a study using about 74% of tax returns to determine how much income was generated by capital assets. As you can see by the chart as time went on the rich got richer and everyone else stayed about the same. Remember that the median income in 2004 was about $43k and in 2007 it was about $48k, which means that about 50% of America is represented just by the two tiny data points on the left of the chart.

These pie charts show the aggregate wealth for the various income tiers quite clearly.

There are a couple of issues in tax law that need to be changed to begin to fix this problem. The first major fix is to treat all income the same. Wages and capital gains should no longer be treated distinctly. Then we need to look at deductions for earning a living. Why should a self employed plumber be able to deduct the cost of her travel expenses to and from various plumbing jobs, while a barista cannot deduct the cost of commuting to and from Starbucks every day he works? Both are trying to earn a living, but the one who earns a living through wages gains no benefit that the businessperson gains. This inequity is very harmful to the working class.

Addressing tax deductions and how we tax differing income types will go along way to helping solve income inequality. But there are more ways we can fix this: looking at flat vs. progressive taxes, and answering the question of whether we should tax income rather than wealth. But this article is enough of a Halloween scare for the rich so I will defer those other topics to another time.